Customer Service

(903) 234-8922

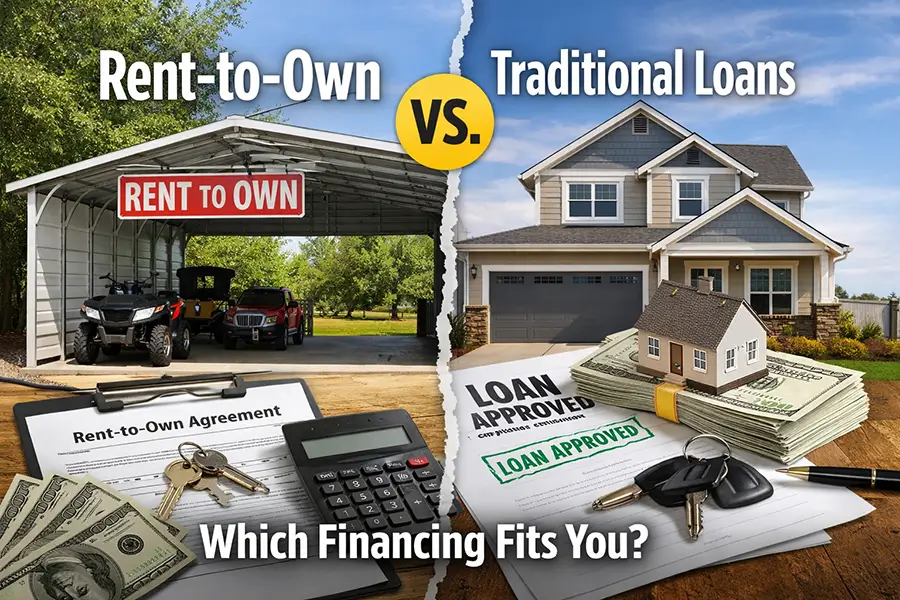

Rent-to-Own vs. Traditional Loans: Which Financing Fits You?

Financing a metal carport, garage, or workshop is rarely one-size-fits-all. For many homeowners and small business owners, the choice comes down to two clear paths: a rent-to-own plan that spreads payments with flexible approval, or a traditional loan that typically offers lower long-term costs but stricter qualification rules. This article breaks down the differences, weighs the trade-offs, and helps you decide which option matches your priorities and financial situation.

How rent-to-own and traditional loans actually work

Rent-to-own programs let you take possession of an item while making scheduled payments that can eventually lead to ownership. Unlike a standard loan, many rent-to-own arrangements have easier qualification, sometimes no credit check, and simplified paperwork. The Federal Trade Commission explains the basics of rent-to-own and related plans, including pitfalls to watch for in contract terms.

Traditional loans — whether a secured equipment loan, a personal loan, or a small-business loan — provide immediate ownership once funds are disbursed, and you repay principal plus interest over a fixed period. Authoritative resources like the Investopedia overview of personal loans and NerdWallet’s explanation of rent-to-own arrangements are useful for understanding timelines, interest, and qualification differences.

Upfront costs and approval: who gets in easier?

If you need a quick solution with minimal upfront cash, rent-to-own often provides the fastest path to ownership. Many programs require only a modest deposit and offer flexible monthly payments that can fit a variety of budgets. This structure makes rent-to-own particularly appealing for buyers who want to install a carport, garage, or workshop immediately without waiting to save a large sum. It also allows homeowners and small business owners to start protecting vehicles, equipment, or inventory sooner rather than later.

For those planning ahead, understanding what to prepare during installation and site preparation is essential. The company’s Understanding Building Components article offers practical guidance on site requirements, foundation preparation, and material considerations, helping ensure that your project starts smoothly and avoids delays.

Traditional loans, on the other hand, usually require stronger credit, proof of income, and sometimes collateral to secure the loan. While the approval process may be more rigorous, qualifying for a conventional loan often results in lower long-term costs due to more favorable interest rates. This can be especially advantageous for larger projects, where the total savings over the life of the loan can be significant. For those considering commercial or sizable residential structures, detailed guidance on selecting the right building size, roof style, and financing strategy can be found in the company’s How To Choose The Right Metal Building For Your Property post, which helps buyers align their financing choice with structural needs and long-term goals.

Total cost: monthly payments versus long-term expense

Rent-to-own arrangements can be easier month-to-month, but they frequently carry higher long-term costs. Because the “rental” component and fees can add up, the total you pay by the end of a rent-to-own agreement may exceed the purchase price plus interest on a conventional loan. Analysts at Bankrate outline typical rent-to-own scenarios and emphasize comparing total outlay rather than monthly affordability alone.

Traditional loans accrue interest that depends heavily on your credit score and loan type. Over a longer loan term, lower interest rates can deliver considerable savings. For a sense of loan types and when each makes sense, review NerdWallet’s guidance on personal loans and cost trade-offs.

Ownership, equity, and flexibility

With a conventional loan, you own the structure from day one. That ownership may allow for tax considerations, resale value, or financing through home equity later. If building longevity and resale value are a priority, the Galvanized Metal Building Construction Manual explains construction choices that preserve value and reduce maintenance needs.

Rent-to-own can feel less permanent until you complete the required payments. Some plans allow early buyout or accelerated payments, but others limit refunds for missed payments. The Investopedia piece on rent-to-own warns readers to read contracts closely and understand the consequences of early termination or missed payments.

Credit, documentation, and timing

If your credit score needs time to rebuild, rent-to-own programs that accept alternative credit profiles may be a realistic path to ownership without waiting. However, if you can qualify for a traditional loan, the paperwork and underwriting can sometimes be worth the better rate. The Consumer Financial Protection Bureau’s resources help compare scenarios where borrowing makes sense versus alternative payment methods and emphasize considering length of ownership when deciding.

When rent-to-own fits best

Rent-to-own may be the right choice when immediate installation is a priority, when credit challenges make traditional financing difficult, or when you prefer a short-term solution with low upfront costs. If speed and flexibility are important, combining a rent-to-own plan with professional site preparation and installation guidance, such as the practical tips offered in the Metal Carport Guide, can help ensure a smoother process and minimize surprises during delivery and setup.

Additionally, planning ahead with these resources allows you to understand site requirements, necessary permits, and any customization options, making the entire experience more predictable and stress-free. This approach ensures that you can enjoy your new carport or metal building quickly without compromising on quality or long-term satisfaction.

When a traditional loan is the smarter option

If you qualify for competitive interest rates, plan to keep the building for many years, or want the long-term cost advantages of lower interest, a conventional loan is often the smarter financial choice. By securing a loan, you gain immediate ownership, which allows you to build equity in the structure and potentially increase the overall value of your property. Long-term ownership also makes it worthwhile to invest in higher-quality materials, durable finishes, and additional features that enhance functionality and appearance. Careful planning during the purchase and installation process can save time and reduce maintenance costs over the life of the building.

The company’s Ultimate Customer Resource Guide offers in-depth coverage of warranties, installation tips, and product considerations that help buyers make informed decisions and maximize the longevity of their metal carport, garage, or workshop. By pairing thoughtful financing with well-planned construction choices, you can enjoy a cost-effective, durable, and high-performing structure for years to come.

Practical decision steps

1. Estimate total cost under both options: Start by calculating the full financial impact of each choice. For rent-to-own, add up all scheduled payments, fees, and any potential early buyout charges to get the true total cost. For a traditional loan, consider the principal, interest rate, and any loan-related fees over the repayment period. Use authoritative calculators from trusted financial sites like Bankrate or NerdWallet to test different scenarios. Comparing these totals side-by-side helps you see which option fits your budget and long-term financial goals.

2. Check approval odds: Understanding your likelihood of approval can save time and prevent surprises. For loans, request pre-qualification or pre-approval to see what interest rates and terms you may qualify for based on your credit profile. For rent-to-own plans, make sure to get all terms, monthly obligations, and any penalties in writing so you can evaluate them fairly against a loan. Resources from the FTC on rent-to-own contracts explain common clauses, hidden fees, and consumer protections to watch for. Knowing your approval odds and the detailed terms helps you make a more informed decision.

3. Factor in non-financial priorities: Cost isn’t the only consideration. Think about how quickly you need the building installed and whether the timeline of a rent-to-own plan or a loan affects your project schedule. Warranty coverage, maintenance support, and quality of materials are crucial for long-term satisfaction, and certain loan or rent-to-own structures may limit or enhance these benefits. Consider your future plans: if you expect to move or sell the property, one financing option may make more sense than the other.

Technical details from construction and component guides, such as those in Understanding Building Components, can tip the balance by showing how installation, durability, and customization options align with your priorities.

Final thoughts

There’s no single “right” answer. Rent-to-own delivers access and speed with lower upfront barriers, while traditional loans usually cost less over time if you qualify. The best choice depends on your credit profile, how long you plan to keep the building, and whether immediate installation outweighs long-term savings. Use the reliable consumer resources linked above to compare costs, and pair that financial homework with the practical building and installation guidance available in East Texas Carports’ articles so you choose a structure and financing plan that work together.

Remember to consider your long-term goals, including potential resale value or future expansion, when evaluating financing options. Think about how each plan affects your cash flow and monthly budget, ensuring it aligns with your financial comfort zone. Also, don’t overlook the importance of warranties and maintenance support, which can make a significant difference in overall satisfaction and peace of mind.

If you’re ready to compare options for a specific project, gather quotes and written financing terms, review construction and warranty details, and then weigh total cost against your timeline and credit options. With the right information, you’ll pick the financing path that fits both your budget and your plans.